A foreclosure is when the homeowner fails to make payments on the mortgage of their home. As a result, the lender reposes the home or asset to repay the rest of the loan.

Texas has two types of foreclosure: judicial and non-judicial. Judicial foreclosures are when the foreclosure is handled through the court system. A non-judicial foreclosure happens outside of the court system. Non-judicial foreclosures are more common.

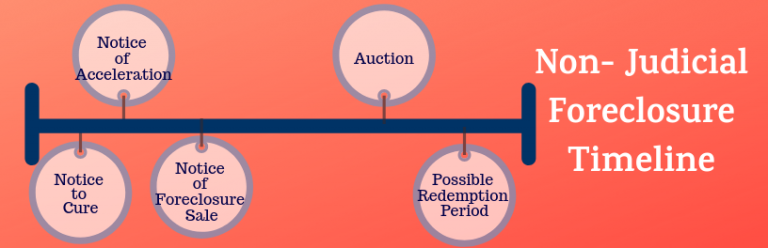

In Texas, the non-judicial foreclosure process can be quick, as little as 41 days. You should be getting two notices from your bank: a notice to default and a notice of acceleration. A lender cannot start the process of foreclosure until these notices are given. You will have 20 days between the notice of default (requires you to pay the past due amount and any fees) and the notice of acceleration (payment of entire amount of mortgage). After the first two notices, you will receive a notice of sale to inform you that your home will be going into foreclosure. This notice will also be the moment that the foreclosure is announced publicly.

The notice of sale will inform you of the date the home will go to auction. You will have at least 21 days between the notice and the day of the auction. You will have the ability to sell your home and forgive your foreclosure up until the home is sold at auction or becomes bank owned, Foreclosure auctions in Texas occur on the first Tuesday of every month.

Some states have a right to redemption that allows homeowners to buy back a house after it has been bought at auction. Unfortunately, Texas isn’t a state that has a right to redemption period. However, tax related foreclosures often include a redemption period.

To learn more about the non-judicial foreclosure process, click here.